PANDEMIC STABILISATION AND RECOVERY FUND

George Kennedy, Partner takes a look at the Pandemic Stabilisation and Recovery Fund.

In brief: The Minister for Finance and Public Expenditure & Reform, Paschal Donohoe TD, announced recently that the Ireland Strategic Investment Fund (ISIF) will make available a new €2 billion fund to support medium and large enterprises in Ireland affected by the COVID-19 crisis.

COMPARISON WITH OTHER COVID-19 BUSINESS SUPPORTS

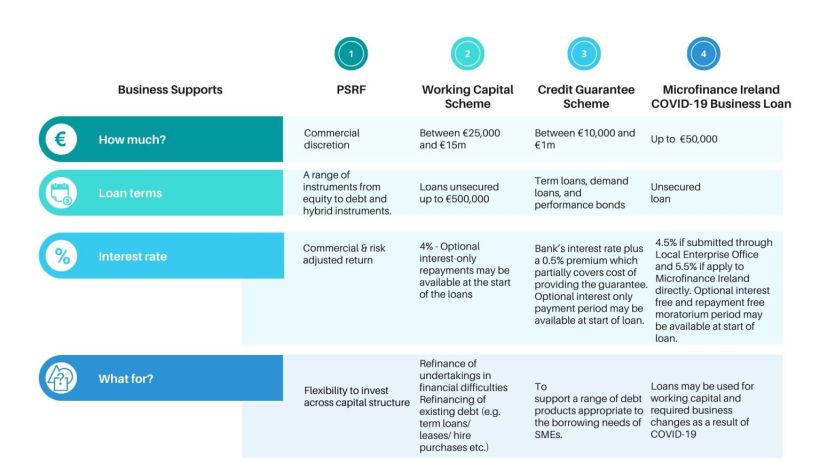

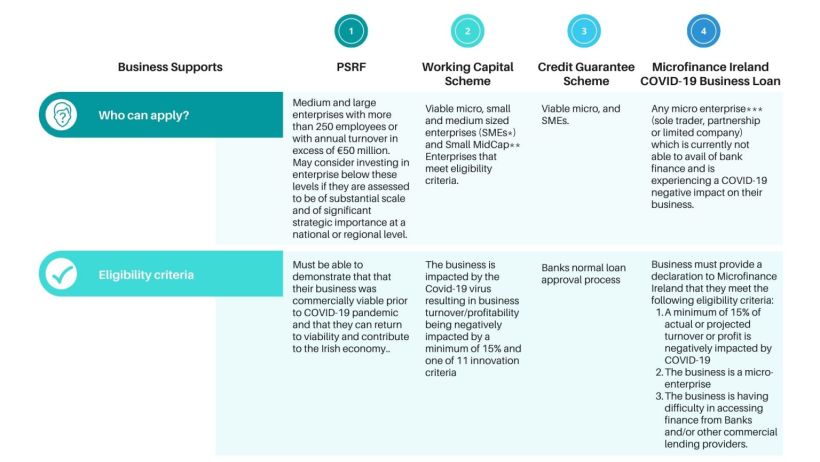

The new “Pandemic Stabilisation and Recovery Fund” (PSRF) is distinguished from the other recent COVID-19 government supports. It will be made available through a sub-portfolio within ISIF and will focus on investing in large and medium sized enterprises, which have more than 250 employees or have an annual turnover in excess of €50 million euros.

POSITIVE NEWS FOR LARGE AND MEDIUM SIZED BUSINESS

ISIF have indicated that they will be flexible in relation to their strategy of investment with the PSRF fund and that they are willing to invest across the capital structure, investing in a range of instruments from equity to debt and hybrid instruments. This will enable businesses to access the capital they require in the most suitable manner for their individual business requirements.

As required under ISIF’s statutory mandate, the PSRF will be invested on a commercial basis seeking an appropriate risk-adjusted return and economic impact from investments it makes with this fund. The purpose of this fund is to create economic stability in the short term and make a reasonable return across the portfolio in the long term. The real benefit to businesses here, aside from the immediate investment, is the timeframe within which ISIF are looking for a return on their investment. While ISIF have indicated that they will pursue a return on investment which will be equivalent to the normal returns sought for this form of capital investment (i.e. 5 to 7 years), ISIF have indicated that they will be flexible with regard to when they seek this return. This reflects the nature of ISIF’s own funding model and is well suited to the uncertainty surrounding the COVID-19 pandemic. ISIF have also indicated that their investment approach will be complementary to other Government policy initiatives, created by other agencies such as SBCI and Enterprise Ireland.

APPLICATION PROCESS

Enterprises must be able to demonstrate that their businesses were commercially viable prior to the COVID-19 pandemic and that they will continue to be economically viable and be capable of contributing to the Irish economy throughout the pandemic and into the future. Businesses will be required to show that they have a strategy which shows a clear pathway to financial recovery. ISIF expect that their typical investment will be between €10m and €50m.

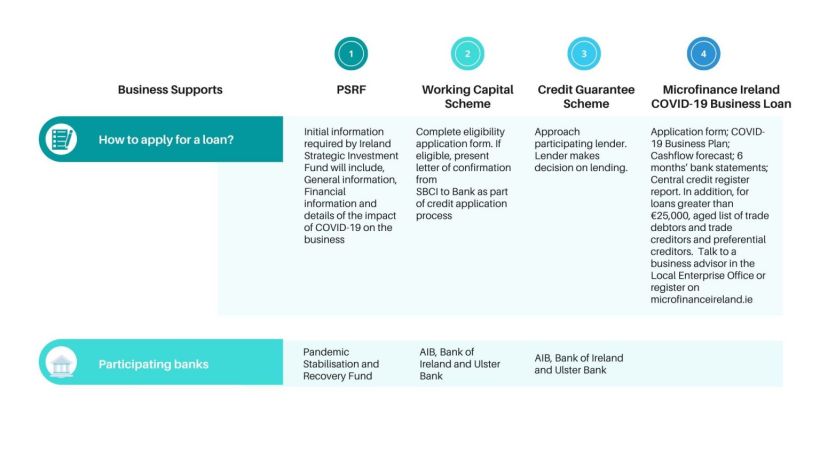

The process by which an organisation can apply to ISIF for investment from PSRF is reasonably straightforward. However, a considerable amount of information needs to be provided. The application process will require information about businesses in three different areas: General information, Financial Information and Impact of the COVID-19 Crisis.

A. GENERAL INFORMATION

The general information required by ISIF comprises the legal and trading name of the organisations, the CRO registration numbers, contact details, corporate structures, the capacity in which the applicants are making their applications and the names of the businesses’ founders, management teams, current shareholders and beneficial owners of shares.

ISIF will also require an in-depth description of how businesses operate, outlining the businesses’ products, markets, unique selling points, customer base and key competitors. The number of employees in each business will also have to be provided, as well as a detailed description outlining if they are employed on a full time or part time basis and whether they are employed in Ireland or overseas. An overview of the geographical footprint of businesses will also be required.

B. FINANCIAL INFORMATION

ISIF also require a large amount of financial information, including a narrative overview of the capitalisation and ownership structures of organisations, outlining any existing debt, key shareholders or any other relevant information. The latest financial accounts filed with the CRO will also be needed, as well as a table showing the organisation`s revenue EBITDA and profit after tax for each of the last 3 years. Documents outlining the organisation`s customer base and concentration, sector exposure and projected turnovers in the next 12 months will also be required for any successful application.

C. IMPACT OF THE COVID-19 CRISIS

Finally, documentation outlining the effects of COVID-19 on individual businesses will also be required. Organisations should state their estimated assessment of capital required from PSRF, as well as the areas where they intend to deploy any new investments within their businesses. ISIF also recommends submitting any business plans organisations have formulated during the COVID-19 crisis.

CONCLUSION

One of the many positives of the scheme is ISIF’s indication that investment will be provided in a quick and efficient manner to companies effected by the COVID-19 pandemic. The purpose of this is to ensure that businesses which were viable prior to the crisis will continue to operate and develop once the pandemic has come to an end. ISIF hope that by providing a speedy roadmap to investment for businesses they can minimise the effect of the COVID-19 pandemic and help the Irish economy recover within the shortest timeframe possible.

*SMEs are defined by the Standard EU definition [Commission Regulation 2003/361/EC] as enterprises that:

Have fewer than 250 employees

Have a turnover of €50 million or less (or €43 million or less on their balance sheet)

Are independent and autonomous i.e. not part of a wider group of enterprises

Have less than 25% of their capital held by public bodies

Is established and operating in the Republic of Ireland

**A Small Mid-Cap is an enterprise that is not an SME but has fewer than 500 employees

*** A micro-enterprise is a business with:

Fewer than 10 full time employees

Less that €2m annual turnover and

A Balance Sheet with Net Worth/ Capital Account / Equity that does not exceed €2m

Related News & Insights

31 July 2026

1 min Min Read

News

Holmes is pleased to have acted for Span...

Edel Conway

Partner

29 June 2026

1 min Min Read

News

Holmes advises on sale of Limerick-based...

Edel Conway

Partner

19 June 2026

3 Min Min Read

Insights

Holmes hosts Professional Negligence and...

Michael Murphy

Partner