HOW WELL PREPARED ARE IRELAND’S BANKS FOR COVID-19?

Going into the pandemic recession banks are assessing their position. Brian McEnery and Harry Fehily crunch the figures

In brief: Irish banks seem to be in a better position facing into the current pandemic crisis as compared to their position entering the 2008 Global Financial Crisis. A number of strategies and policies will assist the Irish banks to weather the storm and assist our economy.

WHERE IS THE BANKING SECTOR NOW COMPARED TO THE 2008 GLOBAL FINANCIAL CRISIS?

In the years running up to the Global Financial Crisis (GFC), Ireland had experienced over inflated asset value on foot of easy credit being channelled through the banking system. This was evidenced by real changes in the decade to 2008 of how Irish banks sourced funds for lending. In 1998, virtually all Irish bank lending was funded by domestic deposits, however in 2008, over half of Irish bank lending was funded by the issuance of bonds on the wholesale market and through inter-bank lending. Increasing valuation of assets and lending at higher levels (LTV) contributed to the crash when it arrived in 2008. This led to the establishment of National Asset Management Agency (NAMA) at the end of 2009 and ultimately the arrival of the Troika in 2011. In 2008, both of Ireland’s large banks AIB and Bank of Ireland had inadequate levels of Tier 1 capital at 5.8% and 5.7% respectively and had the banks not secured Government investment and the most illiquid nonperforming loans (NPLs) of their balance, they certainly would have failed. Unpopular and all as it was, the prospect of depositors losing their deposits if the banks failed would have not just undermined the Irish banks, but the Irish economy also. It was necessary to recapitalise the banks and effectively deal with the quantity of problem loans in the economy.

The scale of the challenge facing Ireland in dealing with NPLs was daunting. These loans for the most part (excluding Ulster Bank) were underwritten by the Exchequer. At the end of 2013, Ireland had the fourth worst level of NPLs in the 30 nations analysed by the European Banking Authority. At that time the European average of NPL to total advances was c. 8%. In Ireland the equivalent number was 25.7%. Only Cyprus, Greece and Romania had a worse NPL profile than Ireland and, for instance, at that time, Italy had a lower NPL ratio of 17.0% NPLs to total advances. In 2011, Ireland had been frozen out of the sovereign debt markets and was dependent on finance from the International Monetary Fund (IMF), European Central Bank (ECB) and the European Commission (Troika).

The establishment of NAMA as a mechanism to resolve NPLs was the subject of much debate at the time and since. NAMA purchased €74 billion (par value) of NPLs for €31.8 billion issuing bonds underwritten by the State and so encashable to bring liquidity to the 5 participating institutions. NAMA then set about deleveraging those NPLs and repaying the sovereign backed bonds as quickly as possible. This was completed in 2017 and the sovereign’s exposure to the NPLs was removed. For sure many of these NPLs are still in existence, because they were bought by private loan acquiring funds, but their recovery is not a financial exposure to the Exchequer. This is relevant as the global economy heads into a second deep recession so soon after the GFC.

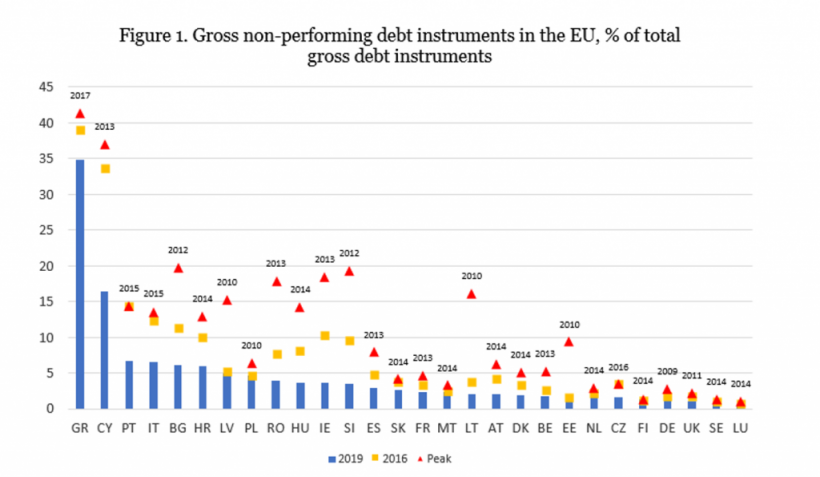

Some other European countries have not achieved what Ireland has and so they roll into a second deep recession with legacy NPL problems. This is before further inevitable NPL problems arise from this pandemic led recession. Across Europe, there were about €543 billion[1] of NPLs at end of quarter three 2019. This is reduced from a level of approximately €1.2 trillion at the end of 2013. NPL levels in Ireland have reduced to below 3.23% (at the end of 2019) from the level of almost 26% at the end of 2013. Other European countries such as Greece (35.15%), Cyprus (16.95%), Portugal (7.17%) and Italy (6.67%) have made progress but not sufficient progress to have a manageable level of NPLs going into this crisis. By comparison the best performing country in the Eurozone is Luxembourg with an NPL level of 0.78%.[2] Graphically, the NPL position across Europe is a set out in Figure 1. This table shows the journey travelled by EU countries in dealing with their NPL problems since the GFC.

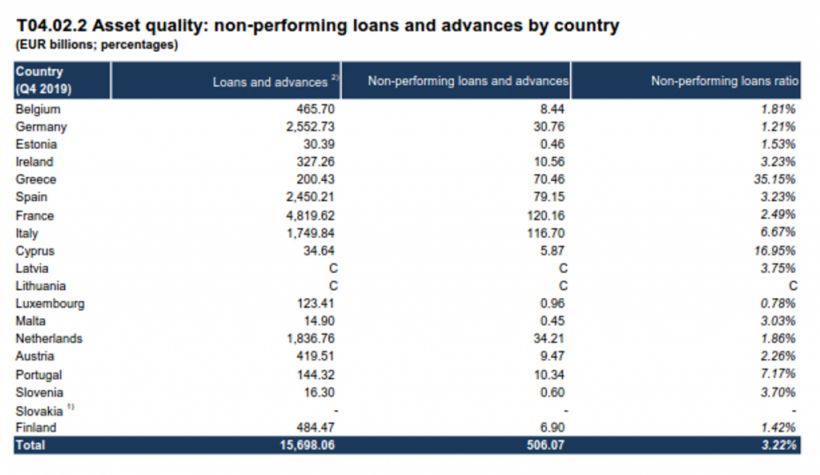

In the images below: The ECB analysis shows that while France has over €120 billion in NPLs this is a small and manageable portion of the French banking system’s total advances. The danger going into the COVID-19 crisis is for countries that have high absolute values of NPLs as well as high NPL ratios to total loans and advances.

In summary on the matter of NPLs in our banking system, Ireland has had remarkable success in deleveraging those from the banking system. NAMA was an important tool in achieving that success and NAMA’s role has been recognised by the European Systemic Risk Board.

HOW WELL PREPARED IS IRELAND’S BANKING SECTOR FOR COVID-19?

Another important factor to reflect upon before answering how well prepared Ireland’s banking sector is for COVID-19, is to examine the strength of the major banks in the economy. Their level of capitalisation is important and this is most frequently measured by a bank’s Common Equity Tier 1 (CET1) ratio. At the end of December 2019, the Irish banks indicated their CET1 levels were as follows:-

AIB: 16.4%

Bank of Ireland: 13.5%

Ulster Ban: 27.0%

Permanent TSB: 15.0%.

The European average for CET1 capital levels at the end of 2019 was 14.78% and so, Irish banks are, for the most part, well capitalised and certainly are in a much better position going into this crisis than going into the GFC. As referenced earlier, the equivalent level of CET1 capital going into the GFC was 5.7% and 5.8% respectively for the two major Irish owned banks.

AIB, Permanent TSB and Bank of Ireland have the State as shareholder to varying degrees. Bank of Ireland has 86% non-State shareholders, while AIB has 29% non-State shareholders and Permanent TSB has the highest State shareholding with 74.92% Exchequer ownership.

THE FUTURE OF THE CRISIS

It is important for the economy that the banks are able to lend by having adequate capital and liquidity to so do. It is vital that the banks have sufficient capital to absorb losses that will inevitably occur from the fall-out of the COVID-19 pandemic, without having to revert to the taxpayer for more shareholder capital.

It is unquestionably important for the banks to support their customers during this crisis and in very many instances to extend credit, or in other instances, to offer moratoria on existing loans. Not to do so is likely to have the effect of worsening the level of business failure and consequently NPLs. However the balance is a delicate one, because banks will be prudent in writing new loans and restructuring existing facilities if they think it is going to result in loan losses. Yet Government wants businesses supported and so the early signs in this crisis, is that to encourage new lending Government is willing to guarantee new loans entirely or to a very high percentage. These measures are aimed to keep credit flowing as well as to avoid banks getting into a similar state as they did 10 years ago. Consequently, we believe Irish banks are in a strong position to weather the storm which is coming.

The more relevant question on this occasion is whether the sovereign will continue to be able to borrow at very tight margins to fund the current budget deficit as well as to implement the capital programme. Over time were this to come into question, then the sovereign as a borrower could have to rely upon the ECB to purchase Government debt. Currently, the ECB is purchasing sovereign bonds and this is unquestionably helping to both minimise and keep the focus away from interest rate spreads between Eurozone countries. How long this can continue is the big question and more importantly what will happen if NPL levels rise in banks in countries like Greece and Italy which have both high levels of NPL as well as high levels of borrowing as a country. A further occurrence of what is referred to as the Sovereign Debt Doom Loop would be very testing for these economies and for Eurozone financial stability.

CONCLUSION

In conclusion many lessons were learned and improvements made after the GFC. Banks are stronger now with higher levels of capital. The issue is that this came with a cost of higher debt for the Exchequer of a number of countries as taxpayers bailed out the banks. A number of European Exchequers and European banks may not have done enough in the short period of good times since the GFC to position themselves for this unexpected crisis. Expect to see more southern European calls for mutualised support and equally expect to see continuing reluctance from northern European politicians and even courts to share in the pain.

This article is co-authored by our Managing Partner, Harry Fehily, and Brian McEnery, Head of Advisory, BDO.

Brian McEnery is Head of Advisory in BDO and specialises in advising on NPL management and work-out structures. He is a former Director of NAMA and is currently advising the Cypriot Government on their NPL Asset Management Company structures and planning.

Source: ECB Annual Report on supervisory activities 2019

Source: ECB Supervisory Banking Statistics, Fourth Quarter 2019

Source: https://www.esrb.europa.eu/pub/pdf/reports/20170711_resolving_npl_report.en.pdf

Related News & Insights

31 July 2026

1 min Min Read

News

Holmes is pleased to have acted for Span...

Edel Conway

Partner

29 June 2026

1 min Min Read

News

Holmes advises on sale of Limerick-based...

Edel Conway

Partner

19 June 2026

3 Min Min Read

Insights

Holmes hosts Professional Negligence and...

Michael Murphy

Partner